From the Larry Connors’ book «Buy the fear, sell the greed», where you can find up to seven high probability trading strategies, I have started to do some research how those strategies have performed since its publication.

To start with, I would like to look at the “Vol Panics Strategy”. The reason I wanted to test this strategy is because I have another strategy which I call “Vix VRP” also trading on the VXX. Here are the rules Larry publishes in his book:

1. VXX is trading above its 5-period moving average and its 4-period RSI reading is above 70. Sell short VXX.

2. Buy VXX on the close if it closes under its 5-period moving average.

The test he covers in the book goes from January 2009 through the end of 2017. He quotes to have a winning probability of 74.04% of the 104 times over the nine years. The average holding period was just under four trading days.

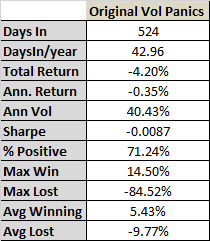

The results are impressive, and I wanted to test it usefulness to incorporate it to our trading plan. To do so, I have done the same from 2009 until the first quarter of 2021. It means adding more than three years to the initial study:

As you can see in the above table, it is truth that the strategy keeps a winning probability of 71.24%; it means we win seven out of every ten signals we get, and we are in the market on average only 43 days per year. The problem comes with the risk: it lost -84.52% in only one trade from 24/02/2020 to 20/03/2020. As Larry points out at the end of the chapter, you always need to respect the market and apply risk management techniques to your positions. He gives two options to do so: to trade VXX on a fixed risk basis either using deep-in-the-money puts or shorting VXX and buying OTM calls.

Therefore, we have an astonishing winning ratio that means nothing without a correct risk management. To overcome this problem, I have looked at my trading strategy I mentioned before to use it as a filter. The reason to use this “Vix VRP Strategy” as a filter is because it goes in and out of VXX by looking at the VIX volatility, so we will only trade the strategy when volatility of volatility is low. So, the new trading rules will be:

1. VXX is trading above its 5-period moving average, its 4-period RSI reading is above 70 and “Vix VRP Strategy” is in short position. Sell short VXX.

2. Buy VXX on the close if it closes under its 5-period moving average.

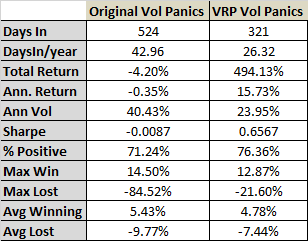

Well, the improvement has been important. By a correct risk management, we can turn a losing strategy into a winning one. Not only we have increased the annual return to a 15.73%, but we have also reduced the volatility by almost a half. We can see it better in the chart below with both equity curves:

What I wanted to show here is that we do not have to trust any trading system by heart without testing it ourselves. Sometimes, a proper risk management is enough to overcome some problems we can face when trading a system. That is what I care about since that is how I trade.